The complexity and breadth of U.S. tax rules can be challenging for investors to navigate. While the intricate nature of the tax code means there is opportunity for investors to capture additional savings, there is also opportunity to make a mistake.

We will work with you and your tax professional to position your investment portfolio to help take advantage of the current tax code.

Here are six common tax mistakes to be aware of, although taxation is just one consideration when making investment decisions.

1. Missing out on savings from tax-advantaged accounts

From 401(k)s to Roth IRAs, there are a variety of tax-advantaged accounts that can help reduce the amount of taxes you owe on your investment earnings. With so many options, it can be difficult to determine which are best for your situation and how to utilize them for maximum tax efficiency.

However, failing to be strategic with these tax-advantaged accounts can cost you in retirement and could result in a higher tax bill.

Avoid this mistake: Make sure you’re making use of the wide array of tax-advantaged accounts available by incorporating a tax diversification strategy into your investment portfolio.

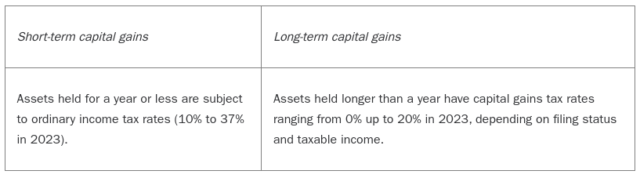

2. Selling an asset before the 1-year mark

Capital gains tax rates vary, depending on the amount of time you’ve held an asset and your annual income. There is a large difference in tax rate if you sell an asset before the one-year mark versus after it. Not factoring these differences into your selling decision can cost you.

Avoid this mistake: In some cases, it can make sense to hold on to an asset until past the one-year mark to get a lower tax rate.

3. Miscalculating your cost basis

In tax terms, the cost basis is the original investment you make in an asset. Your cost basis matters because it will ultimately determine the amount of capital gains tax you pay on the sale of the asset.

Avoid this mistake: When you sell an asset, certain upward or downward adjustments may need to be made to the cost basis, which could affect how much you pay in taxes. Work with my team and a tax professional to track and determine the correct basis in your assets.

4. Neglecting opportunities to harvest your losses

While investment losses aren’t ideal, there are steps investors can take to reduce the sting of poor-performing assets and gain a tax advantage. This strategy, known as tax-loss harvesting, allows you to manage and reduce your tax burden by selling investments at a loss to offset the taxes owed on capital gains from other investments.

Avoid this mistake: Work with my team and a tax professional to ensure you are correctly tracking and reporting your capital losses each year. They can help you evaluate potential opportunities to harvest your losses.

5. Failing to harvest gains

While it may seem counterintuitive, it sometimes makes sense to pay more in taxes now to achieve greater tax savings over one’s lifetime. This is the premise behind tax-gains harvesting, which is the strategic selling of appreciated assets to take advantage of favorable tax brackets that are available to you today. Tax-gains harvesting may make sense for your situation if:

You are presently in a lower tax bracket than you expect to be in the future.

Your capital gains tax rate is 0%, which means you have taxable income less than $44,625 for single filers or $89,250 for joint filers in 2023.

While tax-gains harvesting means your next tax bill may be higher, you may realize greater tax savings than if you had you sold later, when you’re subject to higher tax rates.

Avoid this mistake: Make sure that you are working with a tax professional and financial advisor to evaluate potential opportunities within your accounts.

6. Overlooking state tax planning

Federal tax laws are often top of mind, but don’t forget your state’s tax laws. Many states, for example, tax investment earnings at ordinary tax rates, which can eat away at your gains.

Avoid this mistake: Strategizing for tax efficiency on both federal and state levels can help lessen the impact of taxes on your investment returns.

Reap the benefits of tax-efficient investing strategy

We will account for taxes in your overall investing strategy, and partner with your tax professional to identify strategies that may help you save on taxes.